The Postmark Crisis: How New USPS Sorting Rules Are Threatening Tax Filings and Legal Deadlines in 2026 and Beyond

USPS postmark changes risk late tax and legal filings. Learn why the mailbox rule is failing and how law firms can protect deadlines from regional sorting lags.

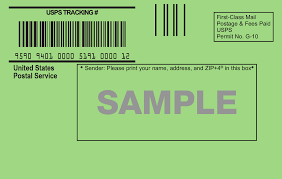

For over a century, the "mailbox rule" has been a cornerstone of American legal and financial life. It is the simple principle that a document is considered "filed" or "sent" the moment it is placed in the hands of the United States Postal Service (USPS), as evidenced by the date stamped on the envelope. However, a quiet but revolutionary change that took effect on December 24, 2025, has effectively ended this era of certainty.

Under the new USPS regulations, a postmark is no longer a guarantee of when you mailed your letter. Instead, it is a record of when a machine at a regional facility finally got around to processing it. For law firms, accountants, and everyday citizens, this shift creates a dangerous "blind spot" that could lead to missed deadlines, rejected tax returns, and legal malpractice claims.

The Technical Shift: From Local Acceptance to Regional Processing

The change is a core component of Postmaster General Louis DeJoy’s "Delivering for America" (DFA) plan, a 10-year initiative designed to modernize the postal network. Historically, mail was often postmarked at the local post office where it was dropped off. This provided a near-instantaneous record of the mailing date.

Under the new rule (codified in the Domestic Mail Manual Section 608.11), the USPS has clarified that a postmark "does not necessarily indicate the first day that the Postal Service had possession of the mailpiece" (USPS, 2025b). Instead, mail is now transported from local "spoke" offices to massive Regional Processing and Distribution Centers (RPDCs). In many cases, these facilities are located hundreds of miles away from the point of origin.

Because the postmark is now applied by automated sorting equipment at these regional hubs, a letter dropped in a blue collection box on a Tuesday might not be processed—and thus not postmarked—until Wednesday or Thursday. This "processing lag" is the heart of the crisis for time-sensitive documents.

Tax Filings and the IRS: The End of "Timely Mailing is Timely Filing"?

The Internal Revenue Service (IRS) relies heavily on the "timely mailing is timely filing" rule established under 26 U.S.C. § 7502. This statute dictates that if a return or payment is postmarked on or before the due date, it is considered on time, regardless of when it actually arrives at the IRS.

With the new USPS policy, this protection is severely compromised. If a taxpayer drops their return in a mailbox on April 15, but the mail is not trucked to a regional facility and scanned until April 16, the IRS will technically view that return as late.

Keegan O’Brien, CPA, notes that this change "could lead to late penalties, interest charges, or rejected filings" for millions of Americans who wait until the deadline to mail their taxes (O’Brien, 2025). The National Society of Tax Professionals has similarly warned that year-end charitable contributions are at risk; a check mailed on December 31 that receives a January 2 postmark may result in a lost deduction for the previous tax year (WebProNews, 2025).

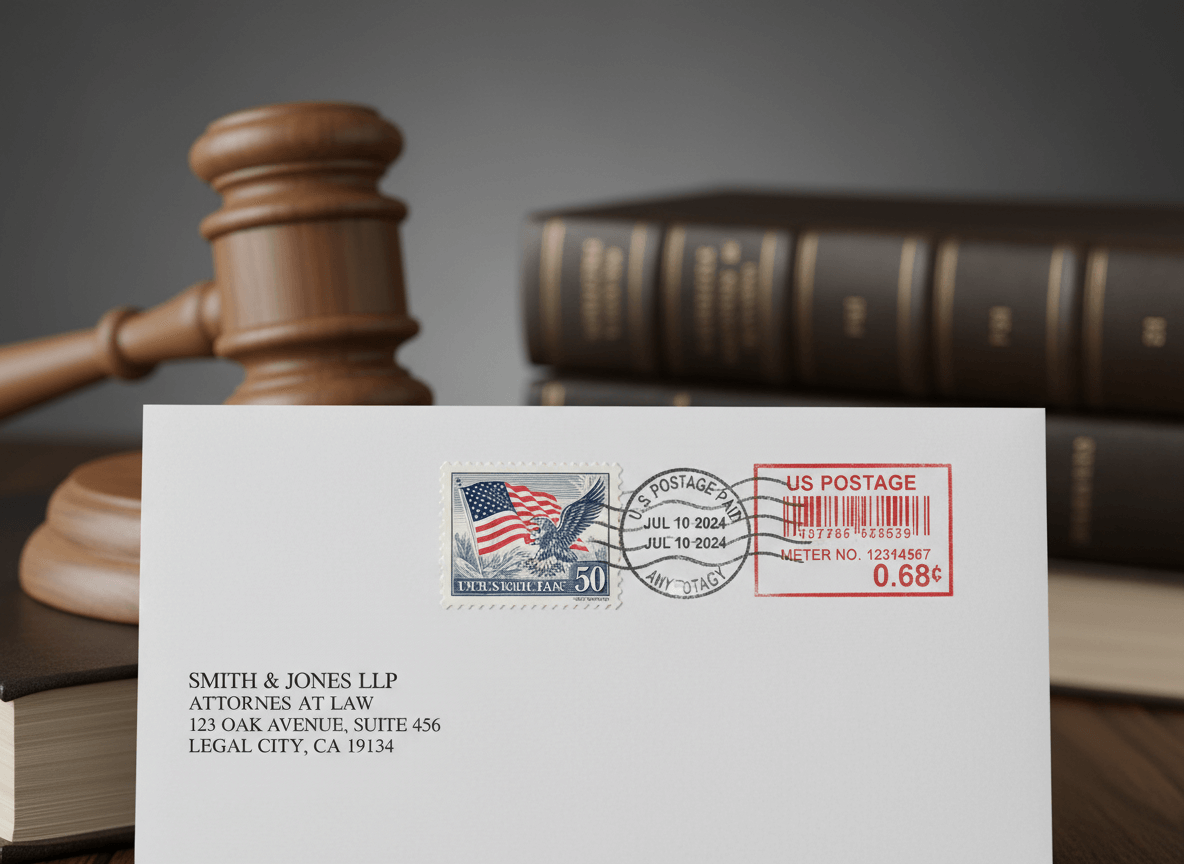

Legal Deadlines and the "Mailbox Rule"

In the legal world, the stakes are even higher. Statutes of limitation, court filing deadlines, and service of process requirements are often strict and unforgiving.

The Breakdown of Contractual and Statutory Deadlines

Most state and federal courts follow some version of the mailbox rule for service by mail. For instance, California and New York have long accepted postmarks as prima facie evidence of timely service (USLegal, 2025). However, if the postmark no longer reflects the date of deposit, the sender bears the burden of proof.

As noted in 27 CFR § 70.305, the sender "assumes the risk that the postmark will bear a date on or before the last date" (Cornell Law, 2025). If the postmark is late or illegible, the sender must produce secondary evidence—such as a certified mail receipt—to prove the mailing date.20 Without this, a case could be dismissed or a motion denied simply because the regional sorting center was backed up.

The LetterStream Dilemma: Risks for Law Firms Using Print-to-Mail Services

Many modern law firms have transitioned to online print-to-mail solutions like LetterStream to handle high volumes of correspondence, such as class-action notices, debt collection letters, and HOA notifications. While these services offer efficiency, the new USPS rules introduce specific vulnerabilities that firms must address.

1. The Indicia vs. Postmark Problem

Unlike traditional mail, services like LetterStream often use a "Postal Indicia" (a printed permit) rather than a stamped postmark. According to LetterStream’s own documentation, "LetterStream mail is processed using a postal permit... this method does not include a visible USPS postmark or date stamp on the envelope" (LetterStream, 2025).

While LetterStream provides internal "Job Mailed" timestamps, these are not the same as an official USPS postmark. In a court of law, a judge may demand a USPS-verified date. If the envelope lacks a postmark and the firm cannot produce a USPS Certificate of Mailing or Certified Mail receipt, the firm may have no way to prove the exact day the mail entered the system.

2. The "Deposit Gap" and Legal Malpractice

When a law firm clicks "Send" on a LetterStream job at 11:30 PM on a Friday, the document is printed and prepared. However, it may not actually be handed off to the USPS until the following business day. Under the new USPS regional sorting rules, that mail might then sit for another 24–48 hours before reaching a facility that generates a tracking "event."

This creates a "Deposit Gap" where the firm believes they have met a deadline, but the official record suggests otherwise. This gap is a breeding ground for legal malpractice claims, especially if a client loses their right to appeal due to a "late" mailing date that was actually caused by a combination of service-provider processing and USPS regional delays.

3. Evidentiary Weight of "Mailing Logs"

LetterStream offers digital mailing logs, but their legal weight is secondary to official government records. Law firms using these services must be aware that if a recipient claims they never received a document, or that it was late, the firm's internal dashboard may not be sufficient to overcome the "presumption of regularity" afforded to USPS official markings.

4. Limited Protection for "Standard" Mail Classes

Law firms often use LetterStream's First-Class options. However, for the highest level of legal protection, "Certified Mail with Return Receipt" is often required. While LetterStream offers these, the cost and complexity increase. Firms that default to standard First-Class mail to save costs are now playing a dangerous game with the USPS's new regional processing timeline.

How to Protect Your Firm and Your Clients

Given the unreliability of modern postmarking, professionals must adapt their workflows immediately.

- Walk it to the Counter: For high-stakes deadlines, the USPS advises customers to visit a retail counter and request a "manual hand-stamp." This is currently the only way to ensure the postmark date matches the day you handed the envelope to a postal worker (Bin News, 2025).

- Use Certified or Registered Mail: These services provide a physical or electronic receipt (PS Form 3800) that acts as "certified" proof of the date of mailing, independent of the postmark applied at a regional center.

- Buffer Your Deadlines: The "last minute" no longer exists. Law firms and tax preparers should aim to mail documents at least three to five business days before a hard deadline to account for the regional transportation lag.

- Electronic Filing Whenever Possible: The simplest way to avoid the postmark crisis is to bypass the physical mail entirely. Most courts and the IRS now offer robust e-filing systems that provide instantaneous, time-stamped receipts.

Conclusion

The shift in USPS postmarking is more than an operational change; it is a fundamental disruption of the legal "chain of custody" for physical mail. As the "Delivering for America" plan continues to consolidate local offices into regional hubs, the postmark will become increasingly decoupled from the act of mailing. For those whose careers and finances depend on deadlines, the message is clear: the blue collection box is no longer a safe haven. It is time to move toward more secure, verifiable methods of delivery before a "late" postmark costs you or your clients everything.

References

Bin News. (2025, December 30). USPS changes postmark rules — and your mail could arrive 'late' in 2026. https://www.binnews.com/content/2025-12-30-usps-changes-postmark-rules-and-your-mail-could-arrive-late-in-2026/

Brookings Institution. (2025, December 30). When a postmark no longer tracks mailing. https://www.brookings.edu/articles/when-a-postmark-no-longer-tracks-mailing/

Cornell Law School. (2025). 27 CFR § 70.305 - Timely mailing treated as timely filing. Legal Information Institute. https://www.law.cornell.edu/cfr/text/27/70.305

Hawkins Ash CPAs. (2025, December 17). Plan ahead: Property tax payments and USPS changes. https://www.hawkinsash.cpa/plan-ahead-property-tax-and-usps-changes/

LetterStream. (2025). Postmark dates - LetterStream help docs. https://help.letterstream.com/article/200-what-postmark-date-will-be-on-my-letter

O’Brien, K. (2025, December 17). USPS postmark rule change: What it means for tax filers and deadlines. JRCPA. https://www.jrcpa.com/usps-postmark-rule-change-what-it-means-for-tax-filers-and-deadlines/

Offit Kurman. (2025, December 18). USPS postmark change: What taxpayers need to know for timely filing. https://www.offitkurman.com/offit-kurman-blogs/usps-postmark-change-timely-tax-filing

Smith + Howard. (2025, December 23). New USPS rule affects mailed tax payments, donations. https://www.smith-howard.com/new-usps-rule-affects-mailed-tax-payments-donations/

USLegal. (2025). Postmark: Understanding its legal definition and importance. https://legal-resources.uslegalforms.com/p/postmark

U.S. Postal Service. (2025a, December 19). Shipping deadlines may be expiring but the postal service “still” delivers! https://about.usps.com/newsroom/local-releases/ca/2025/1219ma-shipping-deadlines-expiring-but%20postal-service-still-delivers.htm

U.S. Postal Service. (2025b). 39 CFR Part 111: Postmarks and postal possession. Federal Register. https://public-inspection.federalregister.gov/2025-20740.pdf

WebProNews. (2025, December 29). USPS postmark rule shift may disrupt tax, election deadlines. https://www.webpronews.com/usps-postmark-rule-shift-may-disrupt-tax-election-deadlines/

Like, share, and follow

Insight is most valuable when it’s shared. If you found these takeaways useful, pass them along to a colleague or friend who is navigating these same challenges. Helping others level up is the hallmark of true leadership. The Best Virtual Paralegal Team loves to share what our team knows so others can grow.

Share

Is your caseload moving as fast as it should?

Holly A. Sheriff, MSLS, MCC, is the Founder and CEO of Best Virtual Paralegal LLC. With over 30 years of experience in the legal industry, Holly specializes in helping personal injury and tort attorneys regain control of their caseloads and keep litigation moving in the right direction.

Alongside her team of veteran paralegals and administrative professionals, Holly provides the high-level support and strategic "momentum" necessary for firms to excel in complex case management. When she isn't helping attorneys streamline their practices, she hosts The Paralegal View podcast, sharing insights on legal innovation and excellence.

Disclaimer and Privacy Polices

The content on this blog is provided by professionals for general information and educational purposes only. It is intended for lawyers, paralegals, and other professionals connected to the legal community in the USA. This information does not constitute legal or other professional advice and should not be used as a substitute for seeking services from a licensed professional.

This content may not reflect the most current legal developments and is not intended as a practice guide. Readers should not rely on this information to answer legal questions concerning actual client situations. All practitioners must consult primary and secondary sources of state law before relying on this information for specific client matters. Best Virtual Paralegal is not responsible or liable for any information provided by the blog's authors or contributors.

Description Title

Authorship: This article was originally authored by Holly A. Sheriff.

AI Assistance: To ensure the highest quality of content and visual presentation, the editorial team at Best Virtual Paralegal LLC utilizes advanced AI technologies—including Gemini, ChatGPT, Galaxy AI, Writing Pro, Grammarly, and Adobe Firefly. These tools are used to assist in editing, refining final copy, and generating illustrative imagery.

Copyright Protection: This content is protected under the copyright laws of the United States. While AI tools are used for enhancement, the creative expression and original insights remain the property of the author and the firm. Copyright protection applies to the fullest extent allowed by law for AI-augmented works.

© 2025 Best Virtual Paralegal LLC. All Rights Reserved.